Handl3r

And in this moment, i swear we are infinite

Basic accounting topic

A story that related to accounting basic

Joe Perez(JP) start a business: a parcel delivery service in his community. He start by run a company Direct Delivery, Inc.(DDI) JP is not have knowledge about accounting so he have advisor Marilyn(M). So M thinks DDI can have thousands of transaction each year -> Accounting software is needed.

Some transactions like:

- Joe will no doubt start his business by putting some of his own personal money into it. In effect, he is buying shares of Direct Delivery’s common stock.

- Direct Delivery will need to buy a sturdy, dependable delivery vehicle.

- The business will begin earning fees and billing clients for delivering their parcels.

- The business will be collecting the fees that were earned.

- The business will incur expenses in operating the business, such as a salary for Joe, expenses associated with the delivery vehicle, advertising, etc.

So start with purpose of the three main financial statements:

- Income Statement(Báo cáo thu nhập)

- Balance Sheet(Bảng cân đối kế toán)

- Statement of Cash Flows(Báo cáo lưu chuyển tiền mặt)

Income Statement(Báo cáo thu nhập)

Income statement will show how profitable(lợi nhuận) DDI has been during the time interval shown in the statment’s heading Profitability involves 2 things:

- Revenues (doanh thu): the amount that was earned

- Expenses (chi phí): expenses necessary to earn the revenues. So in the common, revenues is not the same receipt (Biên nhận) and expenses involves more the just write a check to pay a bill

A.Revenues: The main revenues of DDI are the fees it earns from delivery parcels.

Revenues are recorded when they are earned, not when the company receives the money.

Recording revenues when they are earned is the result of one of the basic accounting principle known

as revenue recognition principle.

(Nói chung là doanh thu được ghi nhận khi mà công ty thực hiện công việc để sinh ra nó chứ không phải chỉ khi nhận

được tiền)

Example: DDI delivers 100 parcels in December for $4 per delivery, he has technically earned fees totalling 400 $

for that month. He sends invoices to his client for these fees and his terms that his clients must pay by January 10.

Even through clients will be paying until January 10, the accrual basis of accounting requires that the $400 be recorded

as December revenues, since that when the delivery work actual took place.

So what will happen on January 10 when DDI receive $400: 400$ of receipts will not be considered to be January revenues,

sin revenues were reported as the revenues of December. This amount will be recorded in the January as a reduction

of Accounts Receivable

B.Expenses: The December income statement should show the expenses incurred during December regardless of when the

company actually paid for the expenses

(Chi phí được ghi nhận khi mà nó thực tế xảy ra để thực hiện công việc bất kể khi nào mà công ty thực hiện trả phí)

Example: J hires someone to help him with December deliveries and J agrees to pay him $50 on January 5. The date

that paid out $50 is doesn’t matter. What matters is when the work is done - when the expense was incurred and in this

case, work was done in December.

The recording of expenses with the related revenues is associated with another accounting principle known as matching

principle.

Summary:The purpose of the income statement is to show a company’s profitability during a specific period of time.

The different between the revenues and expenses for DDI is often referred to as the bottom line and it’s labeled as

the Net Income(Thu nhập ròng) or Net Loss(Lỗ ròng).

Balance Sheet(Bảng cân đối kế toán)

Balance Sheet reflects a specific point of time rather than a period time. So it likes a snapshot of the company’s

financial position.

The Balance Sheet report the amount of company’s (A)Asset, (B)liabilities, (C)stockholder's equity at a specific

point of time

A.Asset(Tài sản): Asset are things that company owns and sometimes referred to as the resources of the company.

Example: Vehicles to delivery, Cash in the bank, Equipment. Vehicles will be reported in Accounts Vehicles, Cash will

be reported in Cash Account. Another type of asset is receivable that will be reported in Accounts Receivable - like

example above, when the deliveries took place but the payment for it will come in the next month.

Prepaid: Another of less obvious asset is the unexpired portion of prepaid expenses. For example, DDI pays $1200 on

December 1 for six-months insurance premium on its deliveries vehicle. That divides out to be $200 per month. Between

December 1 and December 31, $200 worth of insurance premium is used up or expires. The expired amount will be

reported as Insurance Expenses on December’s incoming statement. $1000 remaining of unexpired amount will be reported on

December 31 balance sheet in an asset account

called Prepaid Insurance.

Cost principle and conservatism: The company asset must be recorded with the original cost, and even if the fair

market value of the asset increases, an accountant will not increase the recorded amount of that asset on the balance

sheet. This is result of a basic accounting principle known

as Cost Principle.

But the accountant may decrease asset value as the result of concept known

as Conservatism. Example, DDI decide by purchase 100 packing

boxes to pack the parcel before delivery to client. So it helps DDI to earn more. DDI bought 100 packing box with price

$1 for each box. But after some months, the wholesale price of boxes has been cut by 40% and at today price, he could

purchase them for $0.6 each box. If the net realizable value of his inventory is less than the original recorded cost,

the principle of conservatism directs the accountant to report the lower amount as the asset’s value on the balance

sheet.

(Đại loại là cost principle thì đảm asset sẽ không được báo cáo với mức giá cao hơn giá nguyên bản(cost) của nó.

Conservatism thì đảm bảo asset có thể được báo cáo với mức giá thấp hơn giá nguyên bản của nó).

Depreciation: Some assets are routinely reduced by depreciation. Depreciation is required by the basic accounting

principle known as the matching principle. Depreciation is used for asset wholes life is not indefinite - equipment wear

out.Depreciation is the allocation of the cost of the asset to Depreciation Expense on the income statement over its

useful life. As an example, DDI’s van has useful life of 5 years and was purchased at a cost of $20000. The account

might match $4000($20000/5) of Depreciation Expanses with each year’s revenues for 5 years. So the carrying amount(book

value) will be reduced by $4000 each year that need to be reported in Balance Sheet. So after one year, Balance Sheet

will report the book value of the delivery van as $16000, after 2 years will be $12000. After 5 years- end of van’s

useful life, its carrying amount is zezo.

In summary, depreciation will be reported in the Depreciation Expenses in income statement and carrying amount(book

value) will be report in Balance Sheet.

Accountants view depreciation as an allocation process—allocating the cost to expense in order to match the costs with

the revenues generated by the asset. Accountants do not consider depreciation to be a valuation process.(Đại loại là kế toán sẽ coi khấu hao như 1 cách phân chia cost của asset theo từng giai đoạn để phân bổ nó vào chi phí kiếm ra doanh thu. Khấu hao không được coi như một quá trình định giá nên nó không quan tâm đến giá trị thực tế của asset trên thị trường lúc đó. 1 toà nhà hay mảnh đất có thể tăng giá gấp hàng trăm lần nhưng sẽ không được cân nhắc vào khấu hao hay ghi nhận giá trị thị trường)

One more important point is the balance sheet reports only the assets acquired and only at the cost reported in the

transaction.

(Chỉ những tài sản được acquire và giá trị theo đúng cost của nó trên giao dịch sẽ được báo cáo vào balance sheet. Những thứ như danh tiếng, giả sử như Jeff Bezos sẽ không phải là 1 asset trong balance sheet của Amazon.com)

B.Liabilities(Nợ phải trả): Liabilities are obligations of the company. They are amounts owed to others as of the

balance sheet date (Khoản nợ tại thời điểm lập balance sheet).

Example: The loan J received from his aunt(Notes Payable or

Loan Payable). The interest on the loan he owes to his aunt(Interst Payable). The amount he owes his supplier for items

purchased on credit(Account Payable). The wages he owes an employee (Wages Payable- lương nợ nhân viên mà tính cho giờ

làm việc được trả tính từ thời điểm lập balance sheet).

Another type of Liabilities is money received advance of actually earning the money. For example, suppose that DDI

enters into an agreement with one of its customer stipulating(quy định) that the customer prepay $600 in return(đổi lại)

for the delivery of 30 parcels each month for the next 6 months. Assume DDI receive that $600 payment on December 1, but

it doesn’t have this revenues of $600 because at this time, no delivery for this agreement took place. So the reality

is: the liabilities account involved $600 received on December 1

is Unearned Revenue

or Deferred Account or

Customer Deposit. Each month, as the 30 parcels are

delivered, DDI will be earning $100 and as the result, each month $100 move from Unearned Revenue to Service Revenues.

Each month Direct Delivery’s liability decreases by $100 as it fulfills the agreement by delivering parcels and each

month its revenues on the income statement increase by $100.

(Giả sử cty có hợp đồng trả trước $600 cho 6 tháng tiếp theo delivery 30 parcels 1 tháng thì tại thời điểm nhận đc tiền

vẫn chưa tính là có revenue vì thực chất hoạt động để sinh ra lợi nhuận đó chưa hề diễn ra. Vậy thực chất thì số tiền

$600 nhận được ngay từ đầu sẽ được tính vào Unearned Revenue. Sau đó mỗi tháng sau khi vận chuyển 30 parcels thì $100 sẽ

được chuyển từ Unearned Revenue sang Service Revenue. Mỗi tháng thì mợ phải trả sẽ giảm đi 100$ bên balance sheet và bên

income statement, revenue sẽ tăng thêm 100$).

C.Stockholder’s equity: If the company is a corporation, the third session of a corporation’s balance sheet is Stockholder’s equity. If company is a sole proprietorship(doanh nghiệp tư nhân- 1 người làm chủ), it’s referred as Owner’s Equity. The amount of Stockholders’ Equity is exactly the difference between the asset amounts and the liability amounts. As a result accountants often refer to Stockholders’ Equity as the difference (or residual) of assets minus liabilities . Stockholders’ Equity is also the “book value” of the corporation.

Since the corporation’s assets are shown at cost or lower(not at their market value) it is important that you do not associate the reported amount of Stockholder’s Equity with the market value of corporation.

The account Common stock will be increased when the corporation issues shares of stock in exchange for cash or some other assets. Another account Retained Earnings will increase when the corporation earns a profit. There will be decrease when the corporation has a net loss. This means that revenues will automatically increase Stockholder’s Equity and expenses will automatically decrease Stockholder’s Equity. This illustrates the link between balance sheet and income statement.

(Đại loại là vốn chủ sở hữu sẽ là book value của công ty = assets - nợ phải trả). Tuy nhiên không nên đem vốn chủ sỡ hữu của công ty để liên hệ với giá trị của nó trên market vì theo principle bên trên thì các asset sẽ luôn được ghi nhận <= giá trị thực của nó trên market. Lợi nhuận sẽ làm tăng Vốn chủ sỏ hữu còn chi phí thì làm giảm- nếu revenues > expenses thì sẽ có net income chính là asset tăng thêm -> Có mối liên kết giữa Balance Sheet với Income Statement).

Statement Of Cash Flows(Báo cáo lưu chuyển tiền mặt)

The Statement Of Cash Flows shows how DDI’s cash amount has changed during the interval time shown in the heading of

the statement. Joe will be able to see at a glance the cash generated and used by his company’s operating activities,

its investing activities, and its financing activities. Much of the information on this financial statement will come

from Direct Delivery’s balance sheets and income statements.

The explanation of this statement will be shown later in this post.

Double-Entry System

Double entry is a simple yet powerful concept: each one company’s transaction will result in an amount recorded into at

least two of accounts in the accounting system

(Mọi giao dịch của công ty sẽ phải được ghi lại bằng sự biến đổi trong ít nhất 2 accounts)

I understand that accounting concepts can be difficult to grasp, but let me try to explain the basic idea behind debit

and credit. Debit and credit are accounting terms that represent the movement of money into or out of a business

account. They are used to record financial transactions in a company’s financial statements, such as the balance sheet

and income statement. Debit represents the left-hand side of an accounting entry, while credit represents the right-hand

side. The fundamental accounting equation is Assets = Liabilities + Equity, and every transaction has to keep this

equation balanced. Here is a simple example to help illustrate the concept:

Suppose a company purchases a new computer for $1,000 with cash. The accounting entry to record this transaction would

be:Debit Computer equipment account for $1,000 (asset account), Credit Cash account for $1,000 (asset account).

In this example, the computer equipment account has increased by $1,000, while the cash account has decreased by $1,000.

The transactions have been recorded in accordance with the accounting equation, because the total assets of the company

have remained the same. In summary, debit is used to record an increase in assets or a decrease in liabilities or

equity, while credit is used to record an increase in liabilities or equity or a decrease in assets.

A.The chart of accounts(COA): COA is a list of accounts that will need for report the transaction. So J must found the chart of account that useful to him and his business. Some sample accounts that J will probably need to include on this COA:

- Balance Sheet Accounts:

- Asset Accounts: Cash , Account Receivable , Supplies , Equipment

- Liability accounts: Notes Payable , Account Payable , Wages Payable

- Stockholder’ Equity Accounts: Common Stock , Retained Earning

- Income Statement Accounts:

- Revenue Accounts: Service Revenues , Investment Revenue

- Expenses Accounts: Wages Expenses , Rent Expenses , Depreciation Expenses

B.Sample transaction

- Transaction 1:

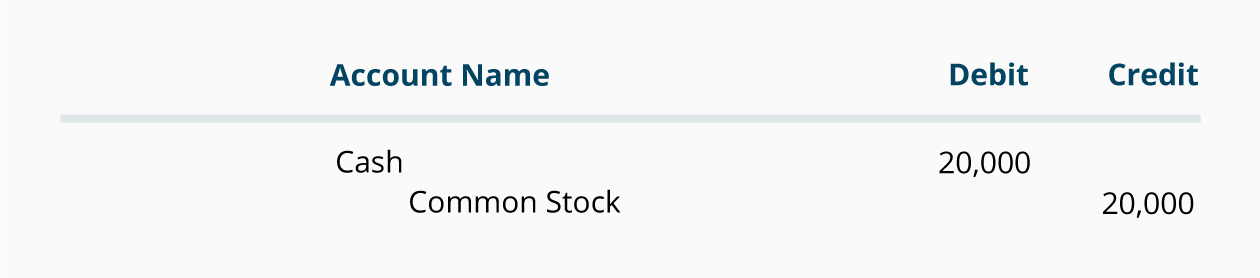

So Joe just start his DDI by his investment of $20000 in exchange for 5000 shares of DDI’s common stock.

- Balance Sheet:

So the Cash Account will increase $20000 and Stockholder’s Equity also increase $20000.

Check the formula:Assets = Liabilities + Stockholder' Equity $20000 = $0 + $20000The accounting equation (and the balance sheet) should always be in balance.

- Debit&Credit

In this case, The asset Cash is increased -> So it should be Debit on the Cash Account.

The Stockholder’s Equity is increased -> So it should be Credit on the Common Stock Account.

- Balance Sheet:

- Transaction 2